Death by a Million Deposits: The New Economics of Check Fraud

Read Time 3 mins | Written by: Karly Field

Paper checks are slowly disappearing. Check fraud isn’t.

That sounds backwards, but the data is unambiguous. Fraudsters are harvesting checks faster than banks are retiring them. On the consumer side, usage is declining. On the criminal side, it’s accelerating.

Fewer checks are being written, but more checks are being sold.

What 2025 Actually Looked Like

When you look at dark-web monitoring data from Finovifi’s FraudXchange across calendar year 2025, the scale of exposure is hard to ignore:

- Nearly 3 million stolen checks surfaced

- More than $39 billion in exposed value

- Over 4,000 financial institutions impacted

- 110,000+ unique payors

- 86,000+ unique payees

- Activity spanning all 50 states

- An average check value around $13,000

- And a single check topping $80 million

This wasn’t a one-month spike or a seasonal blip. Month after month, volume kept climbing. That consistency matters, because it tells us something important: this isn’t a temporary surge. It’s a system that’s working exactly as criminals intend it to.

Why Volume Beats Size Now

One of the most telling shifts in 2025 wasn’t how big individual checks were—it was how many were moving at once.

At roughly $13,000 per item, criminals no longer need six-figure checks to make the math work. They need volume.

That’s the quiet evolution happening in check fraud right now. It’s no longer about one massive hit that lights up every alert. It’s death by a million deposits.

Lower-dollar checks are easier to move, easier to blend into legitimate activity, and faster to deposit. On their own, they don’t always trigger concern. Taken together, they create very real losses—and very real operational strain.

So, What’s Actually Changing?

This shift isn’t accidental. It’s a direct byproduct of how the check ecosystem itself is evolving.

There’s a persistent belief that as checks fade away, check fraud will fade with them. In practice, fraud adapts much faster than payment habits.

Industry research, including analysis highlighted by OrboGraph, shows a clear pattern: overall check volume is declining, but the average value of the checks that remain is increasing. And most organizations are still heavily reliant on paper checks—with no immediate plans to stop using them.

So, while there may be fewer checks floating around, the risk hasn’t gone anywhere. It’s just more concentrated than it used to be. For fraudsters, that concentration is an opportunity.

Where Banks Feel It First

Banks don’t experience check fraud as a chart or a headline. They experience it as a moment.

A deposit comes in.

Someone pauses.

A question gets asked.

A customer conversation follows.

By the time a fraudulent check reaches the deposit stage, the bank is already reacting. Funds may be provisionally credited. Staff time is consumed. Customer trust is put to the test.

What the dark web shows is that many of these checks were circulating long before they ever reached a branch, an ATM, or a mobile deposit channel. The exposure existed earlier—the bank just didn’t have visibility yet.

Why Timing Changes the Economics

This is where things really change. Catching fraud earlier doesn’t just save money—it changes how the situation plays out. Instead of reversals, disputes, and internal scrambling, banks have room to make better decisions. Early awareness gives you options. Late awareness gives you cleanup. And as fraud scales through volume, that timing gap only grows.

The data referenced here comes from Finovifi’s FraudXchange solution, which monitors dark-web marketplaces and criminal channels for stolen check data. By surfacing exposed items earlier in the fraud lifecycle, banks gain insight before deposits, losses, or customer impact occurs.

The Takeaway

As paper checks decline, fraud isn’t fading with them. It’s evolving faster than paper is disappearing. Most banks that struggle aren’t doing anything wrong; they’re just meeting the risk too late in the process. The banks that perform better tend to see it earlier—before a deposit turns into a forced decision. That’s why fraud prevention today isn’t just about spotting fraud. It’s about timing, and what options are still available when risk surfaces. That shift defines the new economics of check fraud.

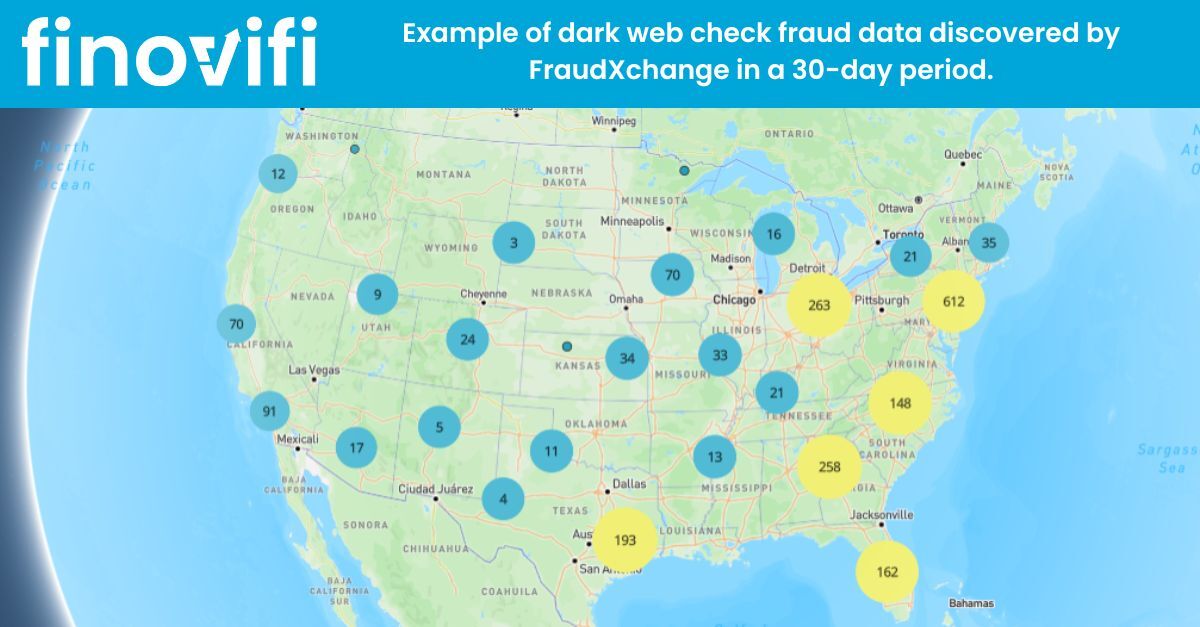

Check out our map of the previous 30-days live check fraud numbers from FraudXchange here.